Imagine that you’ve just gotten your biweekly paycheck. You take it down to the bank and start putting it to work. You haven’t used your bank account for a month or so, so first you check your balance just to make sure everything’s in order. You transfer some money to your savings account or another personal account, then make a cash withdrawal. You get home, and after a brief chat with your spouse, you decide to make your paycheck available to both of you – but, shoot! You left your check stub at the ATM! You need it to be replaced quickly just so you can get on with your bookkeeping, so you put in for an expedited replacement. It arrives, and you turn it into a joint account.

Now imagine that everything that just happened took up 5% of your income.

If you worked a minimum-wage job for Home Depot and got paid with a prepaid payroll card distributed and managed by a third party, then took all of the steps listed above, you spent almost $30 on a $580 biweekly minimum wage paycheck, all because the accessibility of your own paycheck, of the money you worked for, is at the mercy of fees imposed on you by Citibank. That’s almost 5% of an income that is already so low that you can qualify for food stamps even with a full-time job.

Several major media outlets have recently run stories detailing the increasingly widespread practice of paying workers, mostly minimum- or low-wage workers in hourly positions, not with cash, not with direct deposits, but with pre-paid credit cards, and the efforts of workers to fight back against that system. Most of this litigation is in its preliminary stages, is mostly coming from private parties and not the state (the state’s intervention in the wage-card system is so far confined mostly to data-gathering), and is focused not on the wage-card system itself, but on the various fees that come attached to such cards.

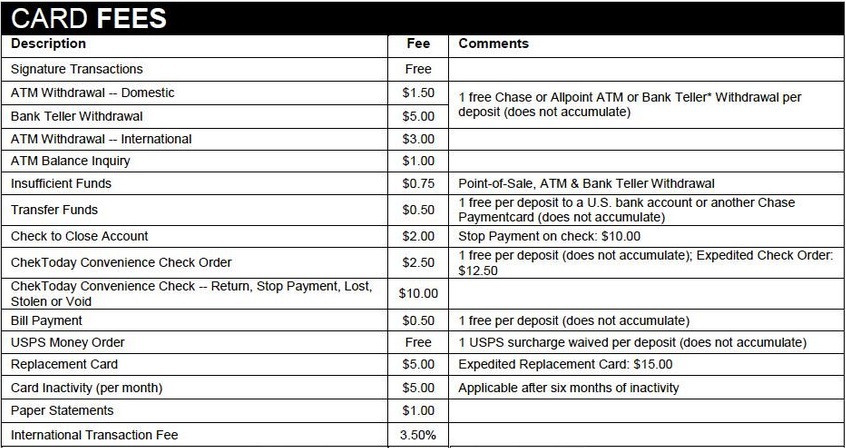

Since the cards are supplied by private parties just like any other pre-paid credit card, the profit motive compels the issuer to build in hefty fees for the kind of transactions that many people with ordinary bank accounts would take for granted. A friend of mine who works an hourly job but who is paid with a payroll card permitted me to share the fee structure she has to deal with just to get access to her own money. Click to enlarge:

Typical prepaid payroll card fee structure

The fees are largely nonsensical – does it really cost the administrator of the card more than three times as much in infrastructure costs if somebody makes a withdrawal from a teller instead of an ATM? Does the card provider really lose money that needs to be recouped if somebody doesn’t use their account for a few months? These questions are not mere rhetorical axe-grinding; there is legal significance to the question of what is being deducted from a paycheck and why (more on that below). And on a minimum wage job, where saving next to impossible anyway, even a few dollars a week off the top can mean the difference between saving for the future and living from paycheck to paycheck. But even one penny to get access to your own paycheck is an intolerable affront to your value as a worker, especially if you’re at the minimum wage level.

Most people are used to seeing such absurd fees in statements for credit cards that they volunteer for, or that they voluntarily reject. But the idea that such a payment scheme can be imposed on a worker from above conjures recollections of the days when employers owned not just the worker’s labor, but the worker’s entire life, when a worker paid in company scrip had nowhere to spend his “wages” at the company store, living in the company dormitories, dying in the company chapel, and being buried in the company funerary lot. The very conditions that gave rise to employment protections in law and the labor movement in general have come back, hidden behind the urbane face of business efficiency.

Clearly, there is something intuitively unpalatable about low-wage workers getting paid with cards that have hefty fees attached to them, even just to access their wages. But is it, strictly speaking, illegal? Millions of Americans are getting paid close to $40 billion a year in wages on these cards by businesses ranging from major retailers to mom-and-pops. Here I’ll give a sketch of why I think that any payments like this constitute wage and hour violations, both in principal and in practice.

I. Requiring workers to accept payment in prepaid credit card format is not paying them “wages” within the meaning of 29 USC § 203(m) and 29 USC § 206(a)

The Fair Labor Standards Act (29 United States Code) is the flagship USC provision on minimum wage, setting the $7.25/hour minimum and defining who’s exempt – tipped workers mainly. To wit, at 29 USC § 206(a):

“Every employer shall pay to each of his employees… wages at… $7.25 an hour.”

Emphasis added. Suppose that, instead of counting off a five, a couple of singles, and a quarter in cash every hour and putting it in your pocket, your employer decided to press a button on a payroll website and change around the numbers on your bank account and hers at the same time – still wages? Uncontroversially yes; electronic wage transfers are easy cases of legal “non-cash” wages. But suppose instead that your employer, instead of giving you either cash or direct deposit, gave you a stack of baseball cards whose net market value averaged out to $7.25, in exchange for an hour of work – still wages? Uncontroversially no; company scrip is dead and employers do not get to unilaterally substitute goods of dubious “real” value for cash. So what about the fuzzy cases in the gray area between the uncontroversial poles – cases like prepaid, fee-laden payroll cards issued in an employee’s name?

For purposes of wage and hour laws, prepaid credit cards are more like a stack of baseball cards than like an electronic direct deposit. Drawing the distinction requires looking at what the relevant distinction is, for wage and hour purposes, between an electronic direct deposit and a stack of baseball cards.

The relevant difference is the cash-like quality of direct deposit versus the non-cash-like quality of a stack of baseball cards, and the wage and hour laws agree. The definition of “wages” in the Fair Labor Standards Act is contained at 203(m), and wages are defined only for the purpose of separating minimum wage-exempt tipped workers from non-exempt non-tipped workers, and in allowing that the Secretary of Labor has the right to determine the value of things like room and board paid in lieu of wages. But the interesting part of the definition of wages here is its emphasis on “cash” for determining how much money a tipped worker should be paid. Tipped workers are allowed to be paid less “wages” than non-tipped workers, where:

“the amount paid such employee by the employee’s employer shall be an amount equal to… the cash wage paid such employee [plus tips]…”

Emphasis added. Now, 29 USC does not define “cash,” but I think that we have a pretty good understanding of why “cash” is the preferred method of compensation. So is a pre-paid credit card cash-like, like a direct deposit, or is it non-cash-like, like baseball cards?

Baseball cards aren’t cash-like because their value is uncertain. There is a specialized market for them that has certain barriers to entry and exit. You can’t trade them into a bank and get a roll of quarters back in value equal to the value of the cards. You have to do something with them before you can buy anything with them, stores and banks are free to decline them as “legal tender” at their leisure. Third-party players control their value, not the state. And a pre-paid credit card is clearly much more like this than it is like cash.

- The value of a pre-paid credit card is highly uncertain. If you have a prepaid card with $50 on it, you’d think you’d be able to buy $50 worth of groceries with it – unless the store doesn’t accept that brand of card, or doesn’t have a card machine. You might lose value on it just by doing nothing whatsoever with it, with an “inactive account fee.”

- There is a specialized market for them that has certain barriers to entry and exit. There are fees to open an account or move money from the card to an existing account. As noted in the fee schedule I showed you above, there’s even a fee to close your prepaid card account in some cases, or to cash it out. You have to pay money just to get rid of the damn thing!

- You can’t trade them and get a roll of quarters back in value equal to the value of the cards because the fees built into the card will give you your roll of quarters minus the costs imposed independently by a third party.

- You have to use the card somewhere, activate it, call a number, sign a form, etc., before you can buy anything with them, and no store or bank in America ever has to accept them as “legal tender.

- And most importantly, the value of the card is determined by a third party, not the state, not the Federal Reserve. What if you get a prepaid Citibank payroll card, and Citibank goes out of business tomorrow? What if Citibank spins off its payroll card service and they start changing around the fee structure after you get the card? What if Citibank spins off its payroll card service and the new company decides that its not going to honor any previous cards?

These are all problems that you have with non-cash instruments that you do not have with cash instruments like cash, checks, or direct deposits.

On this analysis, paying a worker with a prepaid credit card is the baseball card/company scrip model – which is to say, not paying them. A prepaid credit card is illiquid. Its value might drop to zero if Citibank or whoever else administrates or issues the cards goes bankrupt or spins off the division under new conditions. The fees might change. The fees exist at all.

There is caselaw supporting the position that the law treats illiquid, non-cash compensation fundamentally differently from liquid cash or cash substitutes. Smith v. Woodward (2003 WL 23537985) is one of a plethora of cases illustrating this crucial point. Smith, a cattle man, agreed to do work for Woodward’s cattle ranch for a “$2,500 per month labor credit for labor provided.” (Emphasis added by the court but present in the decision.) Woodward ended up paying Smith with $1,000 cash and $1,500 worth of “cattle care services,” and ultimately claimed to the Oregon court that Smith had received his full remuneration since he had received $2,500 in “total value,” but the court disagreed, and found a wage and hour violation. “Cattle care services” are highly illiquid. If you contract to pay someone $2,500 a month, you owe them $2,500 a month, not 2500 “somethings” a month.

A case that shows the same issue from the opposite side is American Airlines v. United States, 204 F.3d 1103 (2000). Hailing from the strange land of tax law, this case saw American Airlines losing an IRS audit over American Express cards it had given to its employees as bonuses following a sudden uptick in business. Airline crews were given $50 vouchers but did not back out taxes from them or report them as payroll taxes, so the IRS pounced and won its case. Sounds like a point in favor of payroll cards, right? Wrong – the only thing that won the day for the IRS was the total liquidity of the American Express cards. The vouchers were good anywhere, they did not specifically name their recipients, they had no fees associated with them, and they were freely transferable. In the court’s own words:

We hold that… the vouchers constituted a cash equivalent benefit. The vouchers were blank American Express charge forms, bearing American’s account number, and in an amount “not to exceed $50.” The vouchers did not contain the employee’s name or any transfer restrictions. Further, although the letter accompanying the vouchers stated that they were only good at restaurants, there was some evidence that they could be used at non-restaurant business establishments. Even if the vouchers were only valid at restaurants, however, they would still be cash equivalents given the lack of restrictions on their use and transferability. According to one of American’s witnesses, the vouchers were essentially bearer paper.

Emphasis added, id. at 1112-1113. “Bearer paper” is basically what a physical check becomes when you endorse it – good as cash for whoever physically holds it. These cases drive home the central thrust of the wage and hour laws’ insistence upon “wages” being paid as “cash,” and “cash” meaning liquidity. Prepaid payroll cards are not that. Prepaid payroll cards are fee-laden, non-transferable, tied to a specific person, without fixed value. Worse, they are often imposed on employees from above as the sole means of compensation, and even where they are not strictly required by the employer, the opt-out procedures are often so complicated that you’d need a JD just to get through the cover sheet.

Unlike an agreement with your bank that gives you a penalty for using certain ATMs, an agreement with your employer is restricted by the Fair Labor Standards Act and all other wage & hour laws. You are free to contract for whatever bizarre fees and penalties you want with your bank only within the confines of your imagination, but you are not free to contract as such with your employer. Even if the only alternative is unemployment and utter poverty, you are never free to contract to work for less than minimum wage, or to voluntarily de-exempt yourself from overtime laws.

II. The fees on payroll cards constitute illegal deductions from paychecks within the plain meaning of 29 USC § 206 and they frustrate the purpose of 15 USC § 1671

Except as specifically allowed or required by law or a court order, no deductions are permissible from paychecks. If you agree to work for a certain amount of money, then receiving anything less is wage theft – a breach of contract by your employer, and an act of conversion and theft, unless you’ve been told that you’re getting a pay cut.

There are some kinds of deductions from your paycheck that you should expect, that that your employer is required by law to deduct in most cases. This is your FICA, Medicare, Medicaid, and Social Security. Often this also includes state taxes. Sometimes the deduction is required by a court order – sometimes in bankruptcy, divorce, or child support arrangements, the court will permit an adverse party to take money directly from your paycheck, and these deductions are legal. The Wage and Hour Division of the Department of Labor has provided a helpful fact sheet spelling out an exhaustive list of all other times that an employer may lawfully make deductions from paychecks:

- when an employee is absent from work for one or more full days for personal reasons,

- sick days without a sick day policy or with a policy that limits sick days,

- jury duty, adjusted for certain state-required compensation,

- fees imposed for violation of a good-faith mjor safety rule with the usual notice requirements,

- unpaid disciplinary suspensions per an established policy,

- when you start or end the job partway through a pay period,

and one not on the Wage and Hour Division’s list that is specifically created by the National Labor Relations Act,

- in accordance with the terms of a collective bargaining agreement subject to the usual minimum wage and overtime laws.

And that’s the complete list. The Department of Labor has always articulated a ruthlessly exclusionary policy that no deductions are legal unless we specifically say they are; it isn’t a list that says “these are examples of legal deductions and so stuff like these are legal,” it’s “everything but these specific things are illegal.”

Now imagine that one day you get your paycheck and you notice that some amount – a tiny amount, maybe just fifty cents – is backed out of your check for “CWC.” You go and ask Boss about the CWC deduction and the cheerful reply is: “Check-Writing Cost, my dear employee. Every pay period we have to go through a whole book of checks just writing paychecks to you guys, so to cover that cost, we’re going to bill you for the price of a paycheck. I mean, come on, its just fifty cents – even on a minimum wage job, fifty cents is just pennies a day!”

Unambiguously an illegal deduction. Unless you have a collective bargaining agreement or have otherwise specifically contracted to let your employer back out the “CWC” and taking out the CWC doesn’t put you below minimum wage or below any overtime pay you’re guaranteed, your employer does not get to dip into your paycheck and just take that money out to cover the cost of check-writing fees.

So when I read a justification for payroll cards like this:

Companies and card issuers, which include Bank of America, Wells Fargo and Citigroup, say the cards are cheaper and more efficient than checks — a calculator on Visa’s Web site estimates that a company with 500 workers could save $21,000 a year by switching from checks to payroll cards… A Victoria’s Secret employee… said it cost her $1.50 just to transfer money from her Citi payroll card to her checking account…

all I can think is, “CWC!” The Victoria’s Secret employee is directly compensating her employer for the employer’s check-writing cost with money that comes straight from her paycheck; the employer has shifted its own costs into the employee and the employer knows it, even though the cost-shifting would likely turn a minimum wage worker into an employee of a wage-violator.

And make no mistake – a fee imposed on making withdrawals from a prepaid payroll card just for getting access to your earned wages is, as an economic reality, identical to a direct paycheck deduction. The employer has just added a single step on top of writing CWC on the pay stub and unilaterally backing out a small but non-zero sum: they’ve had the card’s administrator or the bank write it for them on a card statement instead of a pay stub – but then, since the card is the payment, is there really a relevant distinction between a card statement and a pay stub for employees who get paid with payroll cards?

If the language of the Wage & Hour Division’s guidelines or the National Labor Relations Act aren’t sufficiently precise, then there remains a clearly-articulated public policy against aggressive or needless damage done to workers’ net take-home pay elsewhere in federal law. Title III of the Consumer Credit Protection Act at 15 USC § 1671 clearly lays out Congress’s desire to protect paychecks from excessive garnishment, whether by the state or by private parties:

The Congress finds:(1) The unrestricted garnishment of compensation due for personal services encourages the making of predatory extensions of credit. Such extensions of credit divert money into excessive credit payments and thereby hinder the production and flow of goods in interstate commerce.(2) The application of garnishment as a creditors’ remedy frequently results in loss of employment by the debtor, and the resulting disruption of employment, production, and consumption constitutes a substantial burden on interstate commerce.(3) The great disparities among the laws of the several States relating to garnishment have, in effect, destroyed the uniformity of the bankruptcy laws and frustrated the purposes thereof in many areas of the country.

Now, in fairness, the Consumer Credit Protection Act had direct paycheck deductions to creditors in bankruptcy as its specific targets in mind, but the policy objective is clear and unmistakable: the power of private parties to predate upon employees in the form of wage attachments has grown far too powerful, and that we have good reasons to want to restrict the power of private parties from taking money, even money owed according to the terms of good-faith contractual obligations, out of workers’ pockets.

An agreement between an employer and an employee to receive compensation through a payroll card is exactly the kind of predatory consumer transaction at the heart of the anti-excessive-garnishment regime imposed by the CCPA. The employer and the employee are both private parties making private arrangements for goods and services that impose a de facto garnishment on a worker’s paycheck. Even where that garnishment comes to just a few dollars per pay period, the brunt of this garnishment is disproportionately born by the class of workers most vulnerable to the lost of even a few dollars here and there: the minimum wage or low-paying hourly worker in overcrowded labor markets like retail or food service.

Neither the CCPA nor Fair Labor Standards Act provides a precise definition of what constitutes a “garnishment” except to say that they usually come from the state or from a law, usually tax law. But the laws are very clear about what constitutes a deduction, on the guidelines provided by the Wage and Hour Division’s circulars cited above, and it cannot be seriously argued that there is a major distinction for purposes of minimum wage violation analysis between a “garnishment” by a private company in the form of punishing employees to the tune of a few dollars a pay period just for using a payroll card and a “deduction” in the form of an employer essentially billing its employees for the cost that the employer would normally bear in writing checks or making direct deposits. It is the evil of cutting costs from the coffers of employers and shifting those costs to an employee’s pockets that lies a the heart of a slew of wage and hour laws, not the list of which are the FLSA and the CCPA.

Similar policy articulations abound throughout wage and hour laws and the caselaw interpreting them. Employers can pay tipped workers a pitiful $2.13 an hour – unless the tips don’t get the employee up to minimum wage, at which point the employer pays the difference. Employers can make you pay for the price of getting your uniform cleaned, or can make a security guard pay for his gun – unless the total expense puts the employee below the minimum wage. Nobody is exempt from overtime pay or from the minimum wage – unless the law specifically says so, at which point, the minimum wage is a non-negotiable duty owed to employees.

The unmistakable footprint of this policy abounds in the wage and hour laws. The entire regime of employment law orbits the proposition that one hour of an American’s time is worth not less than $7.25 an hour to an employer. Under the payroll card system, America’s lowest-paid workers find themselves on the receiving end of “fees” serving an economic function identical to illegal wage deductions to cover the employer’s costs of managing a fair, legal payroll system, in open defiance of a clearly-articulated public policy to the contrary – to the tune of $40 billion a year and rising.

III. And if there isn’t already, there ought to be a law forbidding the practice of paying with fee-laden, highly illiquid payroll cards

It is possible that this analysis is all insufficient to establish the case I want to make, that the only reason we’d ever have to think that Congress intended for the minimum wage to truly be $7.25/hour is if it somehow said so more clearly than in the bevy of statutes cited herein. If such is the case, then at the very least it is an essential and imminent public concern to produce legislation clearly forbidding the practice of “paying” workers with non-cash, highly illiquid, fee-laden, wage-draining privately-issued bank scrip instead of money.

The last several decades have seen a relentless assault on the lowest-paid American workers. The courts have almost completely eliminated the power of workers to join together in class-action suits to levy their grievances en masse, in suits that by themselves are too small in winnings and too big in factual complexity for it to be worth any competent lawyer’s time. Wages are stagnant against skyrocketing employer-side profits, and the minimum wage is now so low in terms of real dollars that the minimum-wage worker typically qualifies for food stamps – Wal-Mart is so embroiled in this reality that it even has programs in place to help its workers get on EBT. Meanwhile, years of carefully-calculated public opinion assaults have driven membership in unions, the only social force that has consistently given workers a prayer of balancing the overwhelming lopsided power employers have over low-wage or unskilled workers, to historic lows, and it has taken a near-total collapse of the American middle class to get union favorability back above water. Workers have been told that discrimination is over, that the gender pay gap is motherhood’s fault, that unions are all mafia fronts, that your employer has a divine right to read your social media posts and monitor your email, that business efficiency is all that matters, that those with the hungriest waistlines must tighten their belts the hardest, for decades, and now we have come full circle to the point where employers are issuing private currency systems, for their own benefit, as “compensation” to the economically-powerless underclass they have tired so hard to create.

There is a law. There are several laws. I have cited a small fraction of them here, a smaller fraction still of the case history, showing unmistakably that the payroll card system is an intolerable affront to everything that American wage and hour law stands for. But if somehow when the dust settles from the increasing public and state attention that payroll cards are receiving and the cards remain intact, then our leaders must be petitioned to look back to the days of company towns sustained by company scrip and say “never again!”